TO ALL MEDICAL AND MEDIA PROFESSIONALS

CEASE AND DESIST ORDER

and

NOTICE OF LIBEL

WHEREAS it is a Doctrine of Equity and of Military Law:

There shall be no responsibility without commensurate authority;

and its converse:

There shall be no authority without commensurate responsibility:

NOW THEREFORE, I, Timothy Paul Madden, a being-of-conscience / being-of-equity, acting in good-faith, with sufficient knowledge and understanding-in-fact, do hereby and hereunder invoke the equitable doctrine of necessity to issue the following two orders to all broadly-defined medical professionals worldwide, and to anyone in any directly or indirectly related-business or activity, including and especially the broadly-defined media and those in the pharmaceutical industry:

[ORDER 1] All medical professionals, and media professionals, are to forthwith cease and desist in the use or employment of the deceitful and libellous term “unvaccinated” to refer to people who have not been vaccinated and are not-vaccinated.

People are either vaccinated or they are not-vaccinated, and once vaccinated, in practice, they cannot be unvaccinated.

Calling or labeling someone who has-not-been vaccinated as unvaccinated is not just inaccurate and structurally-dangerous – it is a slander and / or a libel in-fact and a libel in-law.

It is the same well-recognized fraudulent and deceitful form-and-device of or as describing someone who has never been convicted of a crime as being unpardoned or unparoled; or anyone who has not been exposed to radiation as un-decontaminated.

It is also an egregious and fraudulent perversion of the English language and grammar. It is also pejorative, defamatory, inflammatory, and intended to incite hatred against those so slandered or so libelled.

In practice and at its current level, it is being used to mark those so libelled as experiencing diminished intellectual capacity, as evidenced by manifestly irrational delusions founded in paranoia, while the manufacturers themselves operate without insurance, and in express reliance on a government-issued-liability-exemption because the potential liabilities are otherwise too great to undertake.

It also persists as a menace to, and in suppression of, public appreciation of the current and pervasive irreversible nature and fact of the available vaccination procedure(s).

And it is a special or double irreversible nature and danger because all of the experimental substances in fact bear the same risks of the old forms, plus they also actively change the body in irreversible ways that were unknown and not present in the old forms.

With every new nominal vaccination, the producing pharmaceutical corporation is issuing / creating a new unfunded-liability, underwritten-in-fact by the receiver of the vaccination, and without any insurance or financial responsibility of the producer. In fact the only thing backing the liability, other than the assets of the one being injected, is an express disavowal of liability for any injuries, damages, or death.

What is not being discussed at all is the financial-value that is concurrently transferred from the people being injected to the owners of the financial, medical, and pharmaceutical industries. At a potential remaining-lifetime average of $100,000 each, for example (about a total of two weeks hospitalization in the U.S.), there is created a potential $100 billion in future treatment profits, per one-million people injected. The owners get that for free by coercing the masses into de facto mandatory-vaccination or mandatory-submission to the self-declared deciders.

The more comprehensive non sequitur left to the public to contemplate is that the producers of the vaccines demanded legal immunity from government to be induced into producing the product(s), because the potential liabilities were otherwise simply too enormous, while the people who are being vaccinated are told that it is so safe that it is not even worth worrying about, and that anyone who believes otherwise is prima facie suffering diminished-intellectual-capacity – another manifestation of the slander and libel.

And government immunity from civil liability does not change the fact of any tort so committed.

Further, in the presence of criminal-negligence, the effect of the government’s exemption is to attach the personal/equity-liability of the directors, executive officers, and other actual or constructive agents and employees of the producing corporations.

[continued under Note 1, below]

[ORDER 2] All medical professionals, and media professionals, are to forthwith cease and desist in the use or employment of the egregiously-fraudulent and dangerous term “the vaccine” without a direct antecedent or direct and unambiguous reference to precisely identify which substance or purported vaccine is so referenced.

There are at least five materially different technically experimental-substances produced by at least five different corporate manufacturers and using materially different procedures and processes.

It is recklessly-irresponsible and tending toward criminal-negligence for anyone to make reference to any one or more of them as “the vaccine” without an express and explicit reference to precisely identify which of the experimental-substances they are referring.

For any medical-professional to do so – or alleged media-expert to do so – is at a minimum prima facie criminal-negligence.

The aggregate body of purported official information regarding the nominal COVID nominal vaccines is saturated and confounded with at best meaningless purported-information, and even raw-speculation, by reason of vacuous and unsupported references to “the vaccine” without any way to determine which, if any or all, of the experimental substances is being referred to.

In a court of criminal jurisdiction, such omissions constitute prima facie evidence of criminal intent, and that the party propagating the nominal information had no reasonable grounds by which to assert a genuine belief in its truth or accuracy.

At any Nuremberg-like equity proceedings, such would also stand as prima facie evidence that the propagators of the information knew and understood it to be propaganda, and not of substantive content.

And the persistent use of the materially non sequitur term “the vaccine” in reference to two or more separate experimental substances is prima facie evidence of diminished intellectual capacity tending toward the dangerously-incompetent.

Further to the equities, for most people who have not been vaccinated and are not-vaccinated, the first essential and material issue is as to the composition and makeup of the experimental substances that have been labeled and purported as vaccines.

More specifically: Is this particular substance a vaccine at all? If so, is it the whole vaccine? And if so, is it nothing but the vaccine?

All of these issues are side-stepped by the hypnotic-repetition of the words “the vaccine” in pseudo-reference to any or all of them.

ANYONE who fails to comply, attempts to countermand, interferes with the dissemination of, or otherwise acts contrary to, either or both orders is and will remain liable therefore to extra-national proceedings founded in equity jurisdiction, the most prominent example of which proceedings occurred previously at Nuremberg, Germany, in 1946 and 1947.

NOTE 1

FURTHER TO: CEASE AND DESIST ORDER ONE [1]:

Properly defined:

(To) vaccinate is a transitive verb that means: ‘To inject a vaccine into the body of an animal or a human.’

(To) unvaccinate is a transitive verb that means: ‘The as yet theoretical process of removing a vaccine from the body of an animal or a human that or who has been vaccinated. In practice, however, no known animal or human has as yet been successfully unvaccinated, and the most important function and purpose of the word unvaccinated is through a general and specific emphasis and warning to the public that it cannot be done.

The only genuine current public-purpose or public-policy-purpose of the word and verb (to) unvaccinate is to warn and emphasise the fact-of-it to the public that it is not yet possible to be unvaccinated.

Minimum necessary and sufficient facts.

The general form “He is unvaccinated” is gibberish – an incoherent or otherwise non sequitur assembly of words. The word “unvaccinated” is the past-tense of the verb “to unvaccinate”.

Using an irregular tense-pair like run and ran, the same grammar-error yields a conversion from “He has not been running (He has not undergone the process of vaccination)” to “He is not ran or He is unran” (He is unvaccinated)”.

Literally translated it means “He is the past-tense of the process of removing a vaccine from the body”. Any medical professional should be embarrassed to use such an indicator of borderline-illiteracy.

Neither can any medical professional deny close familiarity with the words: Can this procedure be reversed? It is among the most obvious and natural of questions for a potential patient to ask. Yet those who do so in fact here are being vilified.

The only coherent noun form (and which is consistent with the definition of (to) vaccinate) is to describe an animal or a human who has been vaccinated and has then had the vaccine removed from their body. It is prima facie a fraudulent use of language to describe anyone who has not been vaccinated, and has had no vaccine in their body, as unvaccinated.

In fact and in law – it is a slander and / or a libel against anyone who has not been vaccinated and is not-vaccinated. It defines the same essential and material legal elements as describing someone who has never been convicted of a crime as being unpardoned or unparoled; or anyone who has not been exposed to radiation as un-decontaminated.

The idea that is transmitted – and intended to be transmitted – is that being in the state or category of “unvaccinated” is something that is malum in se or evil / wrongful of itself, and which therefore needs to be remedied, and by force if necessary, and without reference to the fact or quality of the substance held out as the vaccine. Whether the substance at issue is a godsend or a deadly-poison becomes irrelevant.

There are two essential and material elements to the issue. One is the fact and efficacy of the various nominal substances at issue. The other is blind or unsubstantiated-in-fact submission to authority.

The pseudo-paradox is that on a certain level everyone knows that it is about blind submission to authority – but the more monumental that truth is to anyone in particular – the more strongly and emphatically they will deny it.

Under the proper and correct rules of English grammar; ‘He has not been subject to injection of the (or “a”) vaccine’ or ‘He has not been vaccinated’ refer to a very different thing than ‘He is unvaccinated’. It is the difference between asserting that: ‘He has been exposed to evil (whatever medical risk attaches to being “vaccinated”)’ is the same thing as asserting: ‘He is evil.’ – and where the accused was never exposed at all.

The only relevant questions are:

Is it an objectively and materially defective use of the word or label ‘unvaccinated’ to describe someone who is ‘not-vaccinated’ in fact, and the answer is Yes, clearly it is.

Is the use of the term intended to harm or cause harm or detriment to anyone so labeled or libelled?, and, here again, the answer is Yes, clearly it is – and does so in fact.

Stop. There.

The libel is complete. The damage is done.

Although not strictly necessary, it is helpful to bear in mind that what could have been done instead is irrelevant to the fact of it. It is no defence to say that you could have found a way to employ the correct term ‘not-vaccinated’ or ‘has not been vaccinated’ while achieving the same result – even if such were possible – which it isn’t. That is the point either way. Whether, and the extent to which, a libel is offensive is determined in reference to the object or the target of it, and not the one advancing it.

When I contemplate the fact that I have not been injected with any of the experimental substances that have been labeled as vaccines, I am focusing on the reasons why, up to and including the otherwise potential of my own death as a consequence.

But when I am actively classified or referred to as being ‘unvaccinated’ I feel incomplete as if I am an abomination and an offence against nature.

I charge that that is an intentional and planned result, and not an unintended consequence of some other process, whether lawful or unlawful.

I object, and I object strongly, to being so manipulated.

Regardless, “He is unvaccinated” is and remains a grammatical-nightmare and cogno-linguistic-abomination.

Either in excess of one-billion speakers of the English language worldwide are making the same compounded-word-meaning-and-syntax-errors – or someone with the capacity to do so is deliberately manipulating and orchestrating language to maintain the masses in a state of material disinformation and inaction (cognitive-paralysis).

The science and scientific-method necessarily and logically recognizes at least

three essential and material states-of-being or potential states-of-being with respect to any given vaccine:

[1] Those who are vaccinated,

[2] Those who are not-vaccinated, and

[3] Those who are unvaccinated after having been vaccinated.

Just as the branch of medicine known as plastic surgery logically recognises the same basic or standard (and ex temporal) three-class-form of patients or potential patients:

[1] Those who have received breast-implants;

[2] Those who have not received breast-implants, and

[3] Those who have had breast-implants removed.

And even though when the first implant surgeries were performed, there were as yet no patients to list under the removed category.

The false-labelling of the not-vaccinated as unvaccinated is a cogno-linguistic-based preemptive-perceptional-strike to deceive people into what is called a false-dichotomy or fictitious-or-illusory binary-choice. The fact that unvaccination or removal of vaccines from the body is not yet technically feasible is not relevant to either the word-meaning or the grammar at issue.

To vaccinate is a verb or process, and its conceptual and linguistic opposite follows the most basic English-language-pair applied to processes, being do and undo. Logically / syllogistically the reverse-process of to vaccinate is to unvaccinate.

It is grammatically-incorrect to use a verb as a noun, and an ordinary speaker or reader of English would normally be alerted to it as such. But by employing or substituting the past-tense of the verb, which is unvaccinated, the mind is tricked or guided into assimilating it as a noun (a state of being) that attaches to the non-existent object of the vaccination (and which did not occur), instead of to the process of its removal (and which also did not occur).

The error is material and objective – and the result of it is to suppress-in-fact the irreversibility of being vaccinated to both those who have been vaccinated and those who have not – and it is being done in reckless-disregard of public safety for uninsured commercial-gain – and that makes it civil and commercial fraud as well as a libel against those who are not unvaccinated but merely have-not-been–vaccinated.

In more simple terms, the present-tense of the past-tense verb unvaccinated is unvaccinate. But that word – unvaccinate – is a very dangerous word to the producers of the various vaccines (nominal substances) precisely due to the fact that it cannot be done – there is no such existing process as unvaccination. It has a plain and unambiguous English-language-meaning, even though such is not yet technically feasible, and that is an obvious impediment to its broadly-defined marketability (i.e., including by force if necessary).

To minimise that danger and impediment, they need to find something-else to attach the word and concept / idea to. But you cannot use a verb defining a process as a noun without the listener or reader being alerted by the awkwardness of it. So instead they use the past-tense of the word – ending in “ed” to accommodate the mind perceiving it as a noun instead of as a verb (because so many English nouns end with a hard “ed” sound).

If the same grammar-errors and substitutions were to be made with an irregular (non-ed-ending) verb-tense pair like run and ran, then the present-tense (‘He is being vaccinated’ or ‘undergoing vaccination’) would be, for example, ‘He is running (down the road)., while the past-tense would become ‘He is ran (down the road) (He is vaccinated).’ But the mind does not recognise the error and substitution as easily when the verb unvaccinate is presented and used in its past-tense of unvaccinated.

But then they have to go to work on your higher cognitive-functions that are most closely related to language skills. They have to convert you from an intelligent well-educated speaker of English who says “He has been vaccinated” to identify someone who has undergone the process of vaccination (and to maintain the foundational noun and verb (and object) relationship(s)), into a lower-order more-Neanderthal-like-being who asserts of the same: ‘He is vaccinated.’ or ‘He is ran.’ instead of ‘He has been running.”

It concurrently transfers and focuses the animosity and latent-anxiety of the masses of people who have been vaccinated against those who have not, and objectifies that hatred in the being of the people who have not been vaccinated, instead of for not having gone through the process.

It is difficult to hate someone for what they are not – and the verb unvaccinated is used incorrectly as a noun so as to convert not-having-been-vaccinated-in-fact into a deplorable moral-defect in the same man or woman who is labelled or marked as-being unvaccinated instead of as not-having-been-vaccinated or not-having-been-injected-with-the-substance-purported-to-be-a-vaccine.

Here again, the statement “He is unvaccinated.” is technically gibberish. It is non sequitur. Unvaccinated is a verb and cannot stand-alone as a noun – You cannot say: “He is a process.” It is your mind that is twisted through cogno-linguistic manipulation until it seems to make sense or is forced to make sense.

Especially for members of the medical profession – the long-term manipulation of language will eventually destroy their ability to meaningfully communicate with other medical professionals. The lawyers and administrators will compel them to always express things in ways that minimize and ultimately deny liability of the lawyers and of the pharmaceutical corporations.

Already and just with the term unvaccinated, a medical professional trying to review and assimilate vast amounts of related information must subconsciously account for and cognitively manage the fact that the word unvaccinated does not mean unvaccinated – it means something else.

Imagine scaling-up the breast-implant industry to the size and significance of the current vaccine and related industries, but where there is no means to distinguish between someone who has never had implants from someone who has had them removed. Everyone is either implanted or unimplanted and there is no distinction to be made.

How would you process malpractice-insurance-claims for either or both procedures, for example, if everyone who had them removed were classified as never having had them implanted?

Well you couldn’t. That’s the point. No competent industry would ever allow such a double-whammy of objectively-contra-labelling with the potential for material future confusion.

Summary

Contrary to the objective rules of English grammar (and a cogno-linguistic bait-and-switch), that verb-in-the-past-tense (unvaccinated) has been assigned and asserted (switched-in) as a label or name (and falsely pretended noun) to and as an identifiable class or classification of people, for the purpose of inciting or escalating hatred against them, or where such incitement is a reasonably-foreseeable consequence of such objectively-inaccurate and fraudulent labelling (and libelling).

It is also a separate and distinct (and actionable) slander and libel intended to baselessly discredit those so libelled as tending toward non compos mentis or not mentally competent to make such decisions for themselves.

And compounded by the fact that the label is applied to an identifiable group whose members are the precise opposite of what the label literally states.

The not-vaccinated are not, and are incapable of being, unvaccinated. But they are directly contra-labelled as unvaccinated which, intentionally or otherwise, also distracts those who have been vaccinated from contemplating the reality that they cannot be unvaccinated.

If you choose to classify them as such, then there are only two classes of people on Earth – those who have-not-been-vaccinated or are not-vaccinated – and those who are waiting-to-be unvaccinated.

But the masses of English-language-speakers are denied that particular view of the same facts, and the implications of it, because the word unvaccinated has been co-opted for some other purpose.

Another manifestation of the problem-in-equity or in-fact is that, prima facie, the single most important and life-altering issue before them is: “What happens if I am wrong, and it was an objective mistake to have allowed this substance to be injected into my body”?

But the masses of those who have been vaccinated have been habituated to deal with that all-important existential reality and question through naked-denial. It is in fact strongly impressed upon them that it is either a moral-failing or a sign-of-mental-illness, or both, for them to have any doubts.

Financial-system-parallel Note:

The technique of using adjectives and verbs as labels or pretended-nouns to deceive humans has been developed and perfected in and by those in the finance business. Its highest and most lucrative form is called the “nominal” method of interest calculation. “Nominal” means “Existing in name only, not real or actual”. The “annual interest rate” that is declared to borrowers in the U.S. is in fact a non-exclusive logarithmic-derivate “of” the interest rate, and not the interest rate itself or at all.

At the current extreme end, about 25 million of the working-poor in the U.S. are paying a total of about $50 billion per year to micro-lenders and payday-loan corporations at average interest rates of about 30,000% per annum, while being told that the rate is only 300% per annum – by using a highly-deceitful and objectively-fraudulent accounting-device that has been prohibited throughout the U.K. since 1971 as civil and criminal fraud on the grounds that it is false and seriously misleading. See TPM – IPS Item 2, below or attached, – The Rate is Nominal – The Fraud is Real.

The following brief excerpt should be sufficient for medical professionals to appreciate what is going on and the cognitive mis-labeling deceit employed in fact (The referenced CBC.ca Consumer Advisory was to warn consumers that the interest rate defined by a loan of $300 with $400 due in 14 days ($300 of principal plus $100 of interest) is 870% per annum, when in fact it is 180,754% per annum):

If you had an effective / real-interest-rate daily-interest-accrual savings account, then it would have to pay interest at an annual rate of 180,754% for you to earn 33.3% over 14 days (i.e., to earn $100 of interest on a $300 deposit over 14 days).

If you go to any medical professional with a virus that grows or propagates at an observed rate of 33.3% over 14 days, they will tell you that its rate of growth or propagation, measured annually, is 180,754%.

If you ask any competent economist for the annual rate of price-inflation if the observed rate is 33.3% over 14 days, they will tell you 180,754%.

And if price-inflation is occurring at 100% per month, also for example, then something that costs $100 today will cost $200 one-month from now, and $409,600 one-year from now, because the annual rate is 409,500% and not 1,200%.

If I were to respond to the reality of it with: “Yes but 100% times 12 is 1,200%, and there are in fact twelve months in a year”, then I would be sent back to junior-high-school for not paying attention and / or for not doing my homework. It is just plain stupid yet this flat-out-embarrassing logic-flaw (systemic confusion of the rate with the amount) has been engrained into the global finance system owned and operated by the same entrenched-money-power that also gains the benefit of the deceit and deliberate mal-education of the masses.

It is only with respect to this uniquely-special-virus called debt-or-loan-interest, that if it grows at an actual rate of 33.3% over 14 days, then the entrenched-money-power that feeds upon it, and otherwise measures financial performance by the basis-point or 1/100th of 1%, will tell you with a straight-face that it is only 870% per annum, even though they are in the business of knowing that it is 180,754% (That is why it is prohibited as criminal fraud in the U.K.).

The same egregiously fraudulent-accounting-device that is recognised and banned as criminal fraud in the U.K. is required by law throughout the U.S. under the 1968 federal Truth in Lending Act (Regulation Z). The de facto “You Must Lie to the Borrower Act” is merely labelled the “Truth in Lending Act”.

It is the same process by which a True-interest-rate-and-GAAP-fraud-concealment-fee is labelled a Lenders-fee and an Entry-fee-for-a-wager is labelled an Application-fee. We are drowning in fraudulent labels in concealment of the normalization of fraud, forgery and racketeering, and unvaccinated is merely the latest vehicle by which to move that agenda forward.

Likewise, global broadly-defined payment-card-issuers receive, recognize, and record, the USD-equivalent of almost $3 billion per day ($3,000,000,000) or more than $1 trillion per year ($1,000,000,000,000) in concealed-credit-charges and hidden-administrative-fees of which the public is near-wholly-ignorant. Why is that? Because they label-it and market-it to the public as a free-loan-system. And it is also a ‘magic’ free-loan-system that pays $400 million a day in Membership Rewards and Air Miles-like kickbacks to card-users worldwide. Card-users are carefully trained never to ask where the money comes from to cover the $400 million a day in kick-backs (about 20% of the gross rake-off).

See TPM – IPS Item 1 – POP QUIZ, below, – on the nominal credit / charge-card business, which demonstrates how systematically and systemically and pathologically the entrenched-money-power lies about virtually everything by calling it something else.

Humanity is not facing a COVID crisis – It is facing a Language-manipulation crisis.

Intellectual-Property-Security (IPS)

The attached pdf (also copied below) consists of three Parts, and is to demonstrate and establish my specific and general competence to issue the subject orders, and to assume the responsibility for those orders.

[1] POP QUIZ on the Credit / Charge-card business

[2] The Rate is Nominal – The Fraud is Real, and

[3] What happened to the $10 trillion?

These three writings are relatively brief and highly expository in nature, so as to (1) support and justify the invocation and declaration of an equitable or equity-emergency (an emergency-in-fact (like a severe storm that threatens a ship at sea)); (2) to demonstrate the manifest incompetence and incapacity-in-fact of the nominal authorities to deal with the emergency; and (3) to expose the near-pathological inability and regardless failure of the de facto and broadly-defined controlling-class to accurately present any essential and material element relating to anything in which it has a financial interest.

The IPS also serves an important probative-function. Most briefly, to test the subject-matter – change the procedures. To test the procedures – change the subject-matter. The latter is what exposes defective procedures or patterns in the modus operandi of any wrongdoers.

Additional and comprehensive writings in support are available at http://werex.org/werex-home/

The three directly-appended writings are copied below, and attached as a pdf also, in the event the linked-website (werex.org), with additional supporting documentation, becomes inaccessible.

With respect to the information on the website, it is helpful and cognitively-efficient, but not essential, to start with the following four essays in the order given (after reading the three copied below or attached as pdfs):

[4] http://werex.org/mortgage-payment-abatement-advisory/

[5] http://werex.org/a-general-theory-of-financial-relativity/

[6] http://werex.org/the-psy-op-goes-on/

[7] http://werex.org/the-normalization-of-fraud-and-forgery/

CEASE and DESIST ORDERS Issued this 29th day of September in the year 2021.

Timothy Paul Madden, in his equitable capacity as a being-of-conscience.

[signed]

TPM – IPS Item 1

POP QUIZ on Credit/Charge-cards

Payments Volume Growth Boosts Visa’s 2018 Earnings; Key Initiatives To Drive Future Value (October 29, 2018): [Still waiting for fiscal 2019 figures – expected to be 12% to 15% greater]:

In fiscal 2018, Visa’s number of cards (including virtual cards) increased by about 80 million to 3.3 billion. The total [gross purchase] volume [throughput] surpassed a record $11 trillion [just for the Visa banks alone], driven by 182 billion transactions during the year. The company’s payments volume growth remained strong across the globe, with double-digit growth (in constant dollars) in all regions except Europe. [forbes.com website, December 17, 2018]

POP QUIZ

Everyone knows that by paying off their credit card balance in full every month that they are effectively receiving a free loan from the card-issuer (by total $ purchase-volume-throughput about 98% of all card-users do so in fact).

Question 1: How are the world’s aggregate credit/charge-card issuers able to pocket the USD-equivalent of about $2 billion a day ($2,000,000,000) in concealed-credit-charges – about $1 trillion ($1,000,000,000,000) roughly every 18 months – making free loans? Explain your answer.

Question 2: Why does it cost as little as 1% or 50 cents to process a $50 credit/charge-card transaction to pay for gasoline, but up to 6% or $30 (60-times-more) to process a $500 credit/charge-card transaction to pay for dinner at an expensive restaurant? Explain your answer.

Question 3: Why does it cost-in-fact less than 2 cents to process a $1,000 debit-card transaction, but up to $60 (3,000-times-more) to process a $1,000 credit/charge-card transaction? Explain your answer.

Question 4: How are the world’s aggregate credit/charge-card issuers able to pocket $1 trillion ($1,000,000,000,000) in concealed-credit-charges roughly every 18 months without all consumers overpaying by $1 trillion every 18 months? Explain your answer.

Question 5: Where do you believe the money comes from to pay for the $400 million a day in air miles and membership rewards programs? Explain your answer.

Question 6: About 10% or $200 million a day of the total is a direct commission or handling-fees from VAT and other government sales-taxes that are run through these accounts. How are roughly 25,000 PhD’s in Economics globally able to remain oblivious to it? Explain your answer.

Question 7: Given that virtually every credit/charge-card transaction prima facie offends up to two dozen criminal-law / racketeering laws, how is it that the broadly-defined justice department of every country in the world fails to prosecute the card-issuers? Explain your answer.

Question 8: Does the minimum $10 billion per year ($10,000,000,000) that is kicked-back directly as rewards to card-carrying judges, lawyers, politicians, political-parties, court-system-workers, and the owners and employees of credit-reporting agencies affect your answer to Question 7? Explain your answer.

Question 9: What allegedly-intelligent species on planet Earth has become so habituated to nominal authority over common sense that it can be systematically looted of $1 trillion ($1,000,000,000,000) every 18 months while genuinely believing something as transparently ridiculous and flat-out-stupid as the free loan story? No need to explain your answer.

POP QUIZ

Short-Answer Key

How much is $1 trillion ($1,000,000,000,000)?

Before reviewing the POP QUIZ Short-Answers, and to grasp the scope and scale of the crimes being committed, it is necessary to first grasp the enormity of the amount of wealth / purchasing-power that is being diverted into the pockets of the entrenched-money-power as an ongoing rake-off from the (mostly-labour-based) income of the masses.

Assume that you need to build, from scratch, (and sell) an automobile that sells for $50,000 in order to obtain $10,000 of gross operating profits. To obtain $1 trillion ($1,000,000,000,000) in such gross operating profits from your productive activities it is necessary to build and sell 100 million (100,000,000) such automobiles!

BMW, to take a closely-representative example and frame-of-reference, has a market value (2019 market cap) of about $25 billion, and directly employs about 135,000 people worldwide. With $1 trillion you could theoretically purchase forty (40) such corporations and all their collective assembly plants and other infrastructure that would employ over five million workers worldwide.

A typical modern major automobile assembly plant working at more or less full capacity will produce about 1,000 new automobiles per day. So assuming 500 production days every 18 months, it would take the equivalent of 200 such assembly plants to produce 100 million automobiles over 18 months – that’s 200,000 such new cars every day.

If the costs could be directly itemized, then there would be or need to be two hundred (200) such automobile assembly plants worldwide, and all associated labour and manufacturing / sub-assembly plants (steel, aluminium, glass, plastics, chassis, tires, engines, transmissions, batteries, electronics, etc., etc.) all working up to 24/7 to produce the output necessary to obtain $1 trillion of gross operating profit.

If the core component inputs (from digging the ore out of the ground to make the steel, aluminum, etc., to pumping the oil from the ground to make the plastics, to obtaining the sand to create the window glass, etc., etc.) represent the same again as final assembly, then it would be necessary to marshal an army of ten million relatively sophisticated industrial employees and artisans to produce and sell 100 million relatively high-end automobiles to obtain $1 trillion of new discretionary economic power.

The entrenched-money-power obtains the same $1 trillion roughly every 18 months not by producing and selling 100 million (100,000,000) relatively high-end automobiles, but by running a few megawatts of electricity each day through an installed computer network that they have built up over a 60-year period, and paid for entirely with a tiny portion of the rake-offs themselves.

So let that sink in for a minute or two. A global computerized-bookkeeping-organization is quietly concealing and skimming the same amount from the global economy, every – single – day, as would require the marshalling of an industrial army of ten million skilled workers at 400 major industrial-scale / world-class factories and assembly plants to produce from scratch and sell 200,000 high-end automobiles, every – single – day.

They also and concurrently harvest (or double-dip for) another circa $500,000,000,000 ($500 billion) (on the same credit) every 18 months as interest-called-interest on outstanding account balances!!!

They then tell the public that the reason they have to charge such outrageously high rates on outstanding balances is that they have to cover their losses from the free-riders who take-advantage-of-them by paying their full balances every month!!!

And all in respect of actual processing costs that are no more than about $10 billion every 18 months. And even that is ten-times-greater than the accumulated inter-generational-family-fortune of the world’s then purportedly richest human and first billionaire Howard Hughes in the early 1970’s.

It is, in essence, a competition among all the card-issuers to see who can tell the most outrageous and in-your-face-stupid-story to the public and get away with it.

And at the end of each 18-month period, the aggregate card-issuers might also send the following group Thank-you Note to their aggregate cardholders:

“Dear Cardholder(s): We sincerely want to thank-you for paying an extra $1 trillion into your accounts over the past 18 months to cover our pretended Merchant Fees as such has given us all an extra $1 trillion ($1,000,000,000,000) to spend on corporate jets, limousines, five-star hotels, vacation-resorts, mansions, beach-houses, Ferraris, Porches, Mercedes Benz’s, yachts, art-works, gold, silver, diamonds, etc., and, above all, Bonuses! Bonuses! Bonuses!

But more than that, because of the unique character of that wonderful thing that we here all know as interest (even though we almost never call it that by name) and because we skimmed the extra $1 trillion from your account-payment-stream, not only did we gain that extra $1 trillion as income and profits, but it was also not applied to reduce the true / actual outstanding balances of your accounts, so that after paying in that extra $1 trillion, you still owe us that extra $1 trillion!!! Hey! Life is great and we really really appreciate you taking advantage of us through our free loan system. Here’s looking forward to another great accounting period and another bonus $1 trillion of your earnings over the next 18 months! (Plus of course all the interest on the $1 trillion from this one)!”

SHORT ANSWERS

Question 1: How are the world’s aggregate credit/charge-card issuers able to pocket the USD-equivalent of about $2 billion a day ($2,000,000,000) in concealed-credit-charges – about $1 trillion ($1,000,000,000,000) roughly every 18 months – making free loans? Explain your answer.

Short answer: They do pocket $2 billion a day as concealed credit charges, but they don’t make free loans. At best they are obscenely expensive loans. The card-issuers are, first, and for obvious reasons, pathologically and obsessively secretive about both the fact and amount of the concealed-credit-charges.

[Update (April 2020) – still waiting / searching for global fiscal 2019 figures, but for US by itself:

Card and Mobile Payment Industry Statistics | The Nilson …

nilsonreport.com:

Visa, Mastercard, American Express, and Discover cards in the U.S. generated $6.698 trillion in purchase volume in 2019, up 8.5% over 2018.

___

Assuming U.S. accounts for 30% of global total, the global total throughput (just for these four card-issuers) would be the USD-equivalent of about $22 trillion. An average 3% Price Discount and corresponding (pretended) Merchant Service Charge (concealed-credit-charge-in-fact) would generate about $660 billion a year or roughly $1 trillion every 18 months – but that does not include the other approximate 25% of card-issuers (gas cards, department store cards, other retail cards, etc.). Nor does it include debit-card fees that are often 20-times greater than actual processing costs (e.g., 40 cents charged versus 2 cents actual cost). The all-in-cost of card-processing-fees (aggregate rake-off) worldwide may in fact already be well in excess of $1 trillion ($1,000,000,000,000) per year.]

They also use the so-called clearinghouses, principally Visa International and Mastercard International, as de facto decoys to suppress public appreciation of the fact that well over 90% of the gross revenue is split more or less 50/50 between the nominal merchant’s-bank and the card-user’s bank. Whenever you see mention of revenues or profits for Visa or Mastercard they are almost always in reference to the relatively minor (but still absolutely huge) amounts retained or redirected to the clearinghouse (which was until relatively recently owned by the same banks / card-issuers anyway).

As an additional cognitive firewall, when it is necessary or unavoidable to make public reference to them, all of the card-issuers refer to them as Merchant-Fees or Merchant-Discount-Fees so as to falsely and fraudulently state or imply that they are paid by the merchants.

The concealed-credit-charges are physically paid to the card-issuer by the card-user at the end of the concealed-credit-charge-accrual-period which the card-issuers call a statement-period or far more commonly a grace-period. The merchants have to agree to the rate and corresponding price discount, but it is the card-users who actually pay them – both in theory and in fact / practice.

Over any significant period it is the corresponding on-going aggregate card-user income that is being harvested. Without that the business it is not feasible (and certainly not at this level).

And all of the card-issuers are legally required to – and do in fact – recognise and record the fees as credit-charges and interest-income received from the card-users and not the merchants. If the card-user does not pay, then the card-issuer never receives the fee at all, and that reality of banking and credit cannot be avoided by a label.

And if you do manage to corner them on it, they will blurt out something like: “It’s not a credit charge – it’s a discount for cash!”. So if a given merchant is required to give a 3% price discount for MasterCard, a 4% discount for Visa, and a 5% discount for American Express, then how much is the price of the merchandise and how much is the discount for cash? Well obviously there is no answer because there is a different concealed-credit-charge depending on the provider of the free-loan.

Questions 2 & 3:

Question 2: Why does it cost as little as 1% or 50 cents to process a $50 credit/charge-card transaction to pay for gasoline, but up to 6% or $30 (60-times-more) to process a $500 credit/charge-card transaction to pay for dinner at an expensive restaurant? Explain your answer.

Question 3: Why does it cost-in-fact less than 2 cents to process a $1,000 debit-card transaction, but up to $60 (3,000-times-more) to process a $1,000 credit/charge-card transaction? Explain your answer.

Short answer: The cost of processing a transaction does not change with the amount or purpose of the transaction. The card-issuers simply adjust their fee-rates (required price discounts) to correspond to the maximum amount that can be concealed within the retail-price-structure of a given consumer-goods-and-services-provider. Margins are very tight for gasoline and so there is only a 1% to 2% concealed price discount for card-users. Price sensitivity at expensive restaurants is much lower and so the restaurant owners have to give up to a 6% price discount in exchange for access.

According to industry-trade-publications it costs the card-issuers less than two cents per transaction. The general attitude is: Look, if the broadly-defined public can be kept almost wholly in the dark, and then if absolutely necessary made to believe the story that it costs 60-times more to process a voucher for an expensive dinner at a high-end restaurant than to process one to pay for gasoline, and 3000-times more to process a $1,000 credit/charge-card transaction than a $1,000 debit-transaction, then why shouldn’t we take advantage of that and gouge them to the nth-degree? Yea, that’s it, we’re not really committing a massive and carefully coordinated global-racketeering-fraud, because our victims deserve to be screwed for being so stupid (for being in a stupor).

The public will believe anything that we tell them, so why not get obscenely and near-inconceivably rich for nothing by telling them lies? After all – who is going to stop us?

Questions 4 & 5:

Question 4: How are the world’s aggregate credit/charge-card issuers able to pocket $1 trillion ($1,000,000,000,000) in concealed-credit-charges roughly every 18 months without all consumers overpaying by $1 trillion every 18 months? Explain your answer.

Question 5: Where do you believe the money comes from to pay for the $400 million per day in air miles and membership rewards programs? Explain your answer.

Short answer: Obviously they are not so able. For the aggregate card-issuers to harvest $1 trillion in concealed-credit-charges every 18 months, all broadly-defined consumers (cash, debit, cheque, credit (whatever)) have to overpay by $1 trillion every 18 months.

The money to pay for broadly-defined membership-rewards and air-miles programs (about $400 million per day or 20% of the gross) comes from the concealed-credit-charges.

This isn’t bleeping rocket science.

Question 6: About 10% or $200 million a day of the total (rake-off) is a direct commission or handling-fees from VAT and other government sales-taxes that are run through these accounts. How are roughly 25,000 PhD’s in Economics globally able to remain oblivious to it? Explain your answer.

Short answer: That some 25,000 PhD’s in Economics globally are able to remain oblivious to it is because most anyone with a PhD in Economics suffers from a severe case of SDS or Systematized-Delusion-Syndrome:

“A “systematized delusion” is one based on a false premise, pursued by a logical process of reasoning to an insane conclusion ; there being one central delusion, around which other aberrations of the mind converge.” Taylor v. McClintock, 112 S.W. 405, 412, 87 Ark. 243. (West’s Judicial Words and Phrases (1914)).

These economists spend their professional careers obsessing over their logical processes of reasoning without it ever occurring to them that they might perhaps want to spend a little time examining their (false) premises so as to avoid insane conclusions like banks being in the free loan business.

Meanwhile, most bankers and their owners are laughing-their-asses-off at us because they make more money skimming the sales-tax revenue than they pay in income taxes! Isn’t that special.

Question 7: Given that virtually every credit/charge-card transaction prima facie offends up to two dozen criminal-law / racketeering laws, how is it that the broadly-defined justice department of every country in the world fails to prosecute the card-issuers? Explain your answer.

Short answer: The hierarchy / superstructure of the majority of nations in the world is comprised of de facto agents of the entrenched-money-power. Just as a convenient starting point, if we could go back in time almost 800 years to the castle of King Edward I (Edward Longshanks), then we would witness a general meeting that went something like this:

King: My Lords, who am I?

One of the Lords: Why thou art king sire.

King: That’s right. And as king, what is my job?

One of the Lords: Well your job is to reign over your kingdom and…

King: NO! My job as king – my real job – is to arrange things today to make absolutely certain that my great-grandson is king seventy-five years from now. And if I succeed, then all of your descendants will also be in the same privileged position as you are now, and it will continue like that forever.

Nothing substantial has changed in the ensuing near-800 years. Virtually everything these people do is to make certain that the little people including and especially the working-poor stay that way forever, so that they and their descendants will lord it over the rest of us, forever.

That is why virtually all truly important positions globally are made by direct appointment. That is why the vast majority of judges are former bank-lawyers or bank-solicitors directly appointed by former bank-directors or bank-solicitors. The entrenched-money-power decides who the people are allowed to choose from in so-called democratic elections, and then those de facto puppets directly appoint the people who occupy the positions that can make a difference. And nobody – but nobody – gets so appointed unless and until the entrenched-money-power has enough on them to make certain that they can be controlled.

The entrenched-money-power has one-year-plans, five-year-plans, ten-year-plans, twenty-five-year-plans, fifty-year-plans,100-year-plans, and quite probably 500-year-plans, and all the money they need to pay for the small armies of analysts and consultants and the all-around-sycophants needed to help them execute those plans, while the average or typical member of the-little-people whose wealth they harvest has at best a five-year-plan based on limited and normally deliberately erroneous / falsified information.

Question 8: Does the minimum $10 billion per year ($10,000,000,000) that is kicked-back directly as rewards to card-carrying judges, lawyers, politicians, political-parties, court-system-workers, and the owners and employees of credit-reporting agencies affect your answer to Question 7? Explain your answer.

Short answer: Yes, absolutely. That’s one important reason why they make the kick-back payments in the first place. Once society’s de facto decision-makers and material administrators are on the gravy-train (and it doesn’t take much) it becomes almost impossible to even get them to see the massive criminality of it – let alone actually do their jobs and act upon it.

It is closely related to the process of looking-the-other-way while the card-issuers wholly ignore the accounting laws and legislative rules on defaults.

Most briefly, this business is so mind-bogglingly lucrative – the greatest free-money-gravy-train in the history of the world – that the only way to control it among the privileged-players (card-issuers) is to require 100% write-offs on any account that has been in arrears for 180-days.

If a card-issuer makes a bad business decision by issuing either too many cards or (reinsuring) too much credit in respect of a given account – then that card-issuer is supposed to suffer the loss as a penalty for its bad business decision.

But their collective answer to that is: “NO! NO! NO! – The little people must never be allowed to form the idea that we are subject to ordinary rules, or that they can escape the consequences of our economic policies.”

That is why they disregard the law and purport to sell the defaulted accounts to debt-buyers for as little as four cents on the dollar even though the administrative overhead of it means that they actually lose money overall by doing so.

Everyone would be better off if they were to simply obey the law and write-off the account. The fact and amount of it would still be reported to the credit-reporting agencies, and the defaulting card-user would still find it commensurately more difficult and expensive to (nominally) obtain credit in the future – but the debt would be gone and everyone involved – and I mean everyone – would be vastly better off. It would also avoid or at least limit cascade-failure to their secured debt like car loans and mortgages.

But to the entrenched-money-power it is better to drive thousands upon thousands of people to abject poverty, despair, and even suicide rather than allow the little people to even form the thought that their betters should be or even might be subject to the same rules as themselves.

Question 9: What allegedly-intelligent species on planet Earth has become so habituated to nominal authority over common sense that it can be systematically looted of $1 trillion ($1,000,000,000,000) every 18 months while genuinely believing something as transparently ridiculous and flat-out-stupid as the free loan story? No need to explain your answer.

Short Answer: Humans.

And, here again, after, say, three consecutive cycles (4.5 years) of skimming $1 trillion every 18 months,[1] and stuffing an extra $3 trillion into their pockets as extra / concealed interest income, their outstanding balance interest rates are so high that their aggregate card-holder base still owes them up to another $5 trillion because of it!

Who could have guessed that working both sides of the street could be so lucrative?

“Yes, technically you paid us that $3 trillion from your labour income, but because we counted it as interest for our account, we didn’t use it to pay down your outstanding balances, and because our rates are so high, you currently still owe us another corresponding $5 trillion.”

Just to be clear, if you take a 4.5-year payment stream and apply it to the same aggregate account balance – less the amount by which that balance has been inflated by the pretended merchant fees, then at the end of the 4.5 year period the difference is not $3 trillion but $8 trillion!!! And it is comprised of the relative extra $3 trillion to earned interest income on the banks’ income statements, plus an extra $3 trillion of outstanding balances because the same $3 trillion that went to interest was not used to reduce the outstanding balances, plus another approximate $2 trillion of compounded interest at the 15% to 20% per annum outstanding-balance-rate for 4.5 years on the ever-ascending-balance-difference.

Although, to be fair, $8 trillion is just the theoretical maximum. In practice the total is only somewhere between $6.5 trillion and $7 trillion because the free-riders who pay in full every month don’t incur the 15% to 20% balance rates but would have used it (the concealed-credit-charges) instead to buy down their other lower-rate mortgage debt, etc.

And even though a reasonably-competent high-school student can easily figure out what is going on from the very figures that the Bankers Association has supplied to the minimum five-consecutive Parliamentary Investigations into the Credit/Charge-Card Industry in Canada over the past 40 years, the appointed members of those Investigative Committees who belong to the same political parties who are receiving direct kick-backs from the concealed-credit-charge revenue have never failed to officially conclude that the Card-Issuer’s official and transparently fraudulent explanation is correct, and that all Canadians need to keep running those purchases through the banks’ free loan system to take advantage of those same banks.

In every case the respective Committee has concluded that the bankers’ public explanation is correct – that they are forced to charge such outrageous rates on outstanding balances because they effectively lose money on every transaction where the card-user pays off their full-balance within the statement / grace-period so as to effectively receive a free-loan from the bank / card-issuer. From the various official conclusions / final-reports:[2]

- the effective yield to card issuers is below the posted rate on credit cards…

- ..someone [“interest payers”] is financing credit card balances that are repaid before the end of the grace period..

- What this discussion does highlight is that the grace period is costly to the card issuer – someone must be paid for the funds used to finance a purchase made with a credit card…

- This practice is obviously costly for financial institutions. The bonus card-users receive by taking advantage of the grace period is a cost to the card issuer….

- So, how do card issuers allow for the cost – the lost potential revenue – from those card-users who take advantage of the grace period?

- That some cardholders receive what is in effect a free loan should not lead others to believe that they too deserve a free loan.

And all Canadians have to effectively pay the multi-million-dollar costs of these so-called government investigations that simply ratify the bankers’ ridiculous stories!!! Same in virtually all other countries around the world.

Meanwhile, just the constructive-trust that just keeps getting larger from over fifty (50) years of flagrantly illegal sales-tax-skimming is now, with interest, well into the multiple-trillions of dollars! Compounded interest charges are a double-edged sword.

So when, exactly, are these technical and actual domestic and international racketeering criminals intending to pay it all back?

Bankers: When pigs fly! We’ll let you know. Meanwhile get back to work! After all, if we are ever held accountable to our criminal-law-violations and offences, then everybody knows that the economy will collapse!! HA! HA! HA! HA! HA! HA! HA! HA!

WARNING! – In the maximum 30 minutes it took you to read this eight-page short-answer-key, the global issuers of broadly-defined payment-cards skimmed another minimum $60 million ($60,000,000) from the global economy.

That sucking-sound you hear in the background is global liquidity and working-capital – the life-blood of commerce – but also of financial-parasites.

You may now return to your regularly-scheduled programming.

TPM – IPS Item 2

The Rate is Nominal – The Fraud is Real

A Black woman among the working-poor is faced with a dilemma. She is its sole wage-earner and has a family to feed. She also has an electricity bill that is past due, and if she does not pay it by the next day, her power will be cut off, and there is $100 in penalties and reconnection-fees that will be added to the bill.

She has been working nights at a second job and is expecting $400 but will not receive it for another ten days.

Her only practical option is one of the local micro-loan or payday-loan stores. She has made some enquiries and the best deal that she can get is $335 cash today for her net $400 paycheck in 10-days. The $65 in total charges seems very high, but it is better than incurring the $100 in total penalties on the electricity bill, and so she takes the deal.

Question: Is it more inherently racist for the payday-loaner to tell the woman that the rate of interest is 708% per annum on the implied assumption that she is not well educated in math, and likely does not know how to do the rate calculation herself?

Or is it more inherently racist to simply tell her the truth that the rate of interest is 64,622% per annum, and that she can take-it or leave-it?

Or perhaps it has little to do with race at all?

If you are among the vast majority who don’t have a clue what I am talking about – then read on, because that in a sense is the whole problem.

The nominal method – Another glitch-in-the-matrix of Financial Apartheid

There is a procedural math-error in the way most lenders and creditors determine interest charges under loan contracts, and which at its current upper-level is so ridiculous as to reveal a total fantasy-fiction-world on a par with that in the film The Matrix.

When the agreed interest rate is absolutely low or close-to-zero, the corresponding math-error-amount is very small. Under the nominal method, so-called, an agreed or stated rate of 3% per annum is converted into a real rate of 3.0416% per annum.[3] Accurately stated, the nominal method is the “Well-it’s-pretty-close-as-long-as-the-real-rate-is-really-low-method”.

In practical terms it means that based on the required monthly payment on a 30-year mortgage, the same mortgage principal amount that is paid off in 30-years at a nominal 3% per annum, is paid off in only 29.75 years at a real 3% per annum.

It works the same on all debt, but a 30-year mortgage is a good and consistent way to demonstrate the significance of the relative differences at different rate-levels. Just think of all debt in the economy as one big rolling 30-year mortgage to appreciate what it means to the bankers and other alleged financial-middlemen.

While it remains what the law calls malum in se or evil / wrongful-of-itself (and a fraudulent act) for a financially-sophisticated lender to cheat a less-sophisticated borrower of any amount using mathematical-trickery, at a stated 3% per annum it is not something that the masses are going to start a civil war over.

At an agreed or stated 6% per annum, however, the nominal method converts it to a real 6.167% per annum. Note especially that by doubling the agreed rate from 3% to 6%, the additional amount or overcharge is increased by just over four-times from 0.0416% to 0.167%. That is because the math-error in the nominal method is an exponential-growth-based math-error.

In practical terms it now means that based on the required monthly payment on a 30-year mortgage, the same mortgage that is paid off in 30-years at a nominal 6% per annum is paid off after only 28.6 years at a real 6% per annum. Now the error and extra amount accounts for an extra 1.4 years of payments and about 8% of all the interest money to be paid over the 30-year period.

Now, at this point we hit a kind of general historical limiting-factor because for about its first 100-years the Bank / Banking Act, at various times, limited the rate of interest on a nominal bank loan to a maximum of either 6% or 7% per annum.

Up until this point the general approach had been for the financial-people to admit the fact of the difference while avoiding any discussion of its fraudulent substance, and by asserting that the difference is trivial. Testifying in Canada under oath before the Select Standing Committee on Banking and Commerce in 1928, for example, the spokesman for the private chartered banks (Mr. M. W. Wilson) said of the nominal method discrepancy / overcharge:

Mr. Wilson: It [use of the nominal method] makes an infinitesimal difference. That is not the reason it is done, I give you my word for it. (Parliament of Canada – Select Standing Committee on Banking and Commerce hearing transcripts, [1928] p. 464.)

Likewise the (mostly banker-written) Encyclopedia of Banking and Finance (Munn, Glenn G. Gen. Editor) technically acknowledged the fact of the math-error, and of the at-least-constructive fraud, in its 1937 Edition under the general heading of Interest:

…if the interest period is less than one year, the [amount of interest determined under the] nominal…interest rate is greater than the true interest rate… Practically, however, the difference is disregarded.

Really? Can anyone seriously imagine bankers disregarding a factor that at-the-time accounted for up to 8% of all the interest money to be paid on a mortgage or any other loan over its entire 30-year term?

Let us now regardless continue into the post-1968 era after the interest rate limits were removed from the Bank Act. And bearing in mind that bank Prime in Canada peaked at a nominal 22.75% in August of 1981. And at 20.5% in the U.S., also in August of 1981.

By a stated or agreed 15% per annum, the nominal method increases the real rate to 16.1% per annum and the math-error or overcharge is now 1.1 percentage points or 6.65-times greater than at a stated or agreed 6%. At this level, a two-and-a-half-times (2.5-times) increase in the stated rate from 6% to 15% results in a 6.65-times increase in the relative math-error.

In practical terms it now means that based on the required monthly payment, the same mortgage (or aggregate debt) that takes exactly 30-years to pay off at a nominal 15% per annum, is paid off in only 18.7 years at a real 15% per annum.

The math-error and fraud now increases the total amount of interest money to be paid under the contract by 93%, per se, and accounts for 48% of all the interest money to be paid over the entire 30-year period. By a stated 15% per annum, we have reached the fringe of what is called the exponential-runaway-point.

Still think the bankers maybe haven’t noticed?

At about this point, in 1974, three critical events occurred.

The first is that in the U.K., the U.S. and Canadian nominal method was recognised and banned as civil and criminal fraud on the grounds that it is “false and seriously misleading”; and which was itself the understatement of the century.

The second is that creditors in the U.K. more or less immediately reacted to it by switching to a different but equally criminal means of achieving the same result. Whatever it took to avoid declaration or disclosure of the real interest rate to the people whose wealth they were harvesting by criminal means.

And third is that there was no material public recognition of it in the U.S. or Canada. No screaming headlines like:

U.K. bans U.S. method of interest calculation as criminal fraud!!!

The same families who were (and remain) the primary owners of both the banks and the broadly-defined media decided that the public had no pressing need-to-know – and the creditors in both countries simply carried on systematically lying about the real interest rate as if nothing had happened.

When the nominal / alleged U.S. Fed Rate peaked at 20.5% in August of 1981, the same mortgage (or total debt in the economy) that takes 30 years to pay off at a nominal 20.5%, is paid off in just 13 years at a real 20.5%. Based on the identical physical contract, if the lender merely claims to have interpreted the agreed interest rate as nominal and not real, then the borrower is condemned to pay three times as much interest money on a 30-year debt that is technically paid off in-full by the same monthly payment after 13 years at the same real rate.

And yet the then equivalent of what is today 25,000-plus PhD’s in Economics worldwide remained oblivious to it. How is that even possible?

This cognitive-cancer then regardless continued to metastasize near unabated through the 1980’s until I challenged it in the Canadian Courts in 1989 on the grounds of its prima facie fraudulent substance.

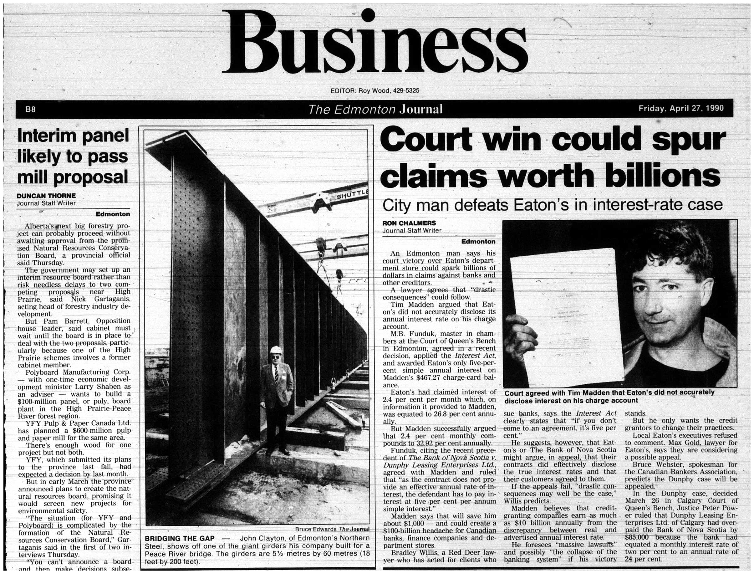

In April of 1990 I won the case (Edmonton Journal, April 27, 1990):

(Note: There is an error / typo by the reporter – “26.8” in the fifth paragraph should read “28.8”)

But my legal win in the Courts was relatively short-lived.

It was fully and finally negated / overturned at the Supreme Court in Canada in 1995 after the lawyers realised that if allowed to stand it was going to cost the banks and the legal profession in Canada a minimum of $100 billion in refunds and write-downs just to pay back the overcharges, and as much as $1 trillion ($1,000,000,000,000) if all creditors in Canada were restricted to 5% per annum for non-compliance as provided under the federal securities law of 1897 that had made the nominal method illegal without concurrent disclosure and declaration of the real interest rate.

The (Hansard) Parliamentary records of debate also make it clear that the legislators in 1897 recognised the nominal method as fraudulent when they enacted the law against it (that was the whole point of the new law). Such also directly defeated the creditors’ official position in my case that there are two equally valid ways of doing it, and that the creditors merely choose the one that is more advantageous to themselves.

Because the creditors had then been simply ignoring the federal securities law for almost 90 years, their lawyers and their malpractice / negligence underwriters would become co-liable for all of the constructive losses and costs of paying it back.

And so aided and abetted by the former-bank-lawyers who had been directly appointed or elevated as judges to the Appellate Courts and the Supreme Court by the former bank-director (Brian Mulroney of the Canadian Imperial Bank of Commerce (CIBC)) then occupying the Office of the Prime Minister, the entrenched-money-power led us to cross the Rubicon and into the Financial Twilight-Zone of modern Payday-Loans and Micro-Loans.

As a general frame-of-reference, between a stated rate of 1% per annum and a stated rate of 30% per annum, the relative error in the nominal method increases exponentially by a factor of (almost exactly) 1,000-times. It is 1,000-times greater at 30% than at 1%.

Above that it gets ever more disturbing, and in several different ways.

Consider the following (and typical) CBC (Canadian Broadcasting Corporation) article nominally advising Canadians on the high cost of payday-loans (cbc.ca website, Payday Loans: Short-term money at a hefty price. October 4, 2006) (in material part, emphasis added):

How much do payday loans cost?

They are the most expensive legal way to borrow money

.…

Typically, you can expect to pay up to $100 in interest and fees for a $300 payday loan. The Financial Consumer Agency of Canada says that amounts to an effective annual interest rate of 435 per cent on a 14-day loan [33.3% for 14 days].

The interest rate objectively defined by that transaction is 180,754% per annum.

If you had an effective / real-interest-rate daily-interest-accrual savings account, then it would have to pay interest at an annual rate of 180,754% for you to earn 33.3% over 14 days (i.e., to earn $100 of interest on a $300 deposit over 14 days).

If you go to any medical professional with a virus that grows / propagates at an observed rate of 33.3% over 14 days, they will tell you that its rate of growth or propagation per annum is 180,754%.

If you ask any competent economist for the annual rate of price-inflation if the observed rate is 33.3% over 14 days, they will tell you 180,754%.

And if price-inflation is occurring at 100% per month, also for example, then something that costs $100 today will cost $200 one-month from now, and $409,600 one-year from now, because the annual rate is 409,500% and not 1,200%.

If I were to respond to the reality of it with: “Yes but 100% times 12 is 1,200%, and there are in fact twelve months in a year”, then I would be sent back to junior-high-school for not paying attention and / or for not doing my homework. It is just plain stupid yet this flat-out-embarrassing logic-flaw (systematic confusion of the amount with the rate) has been engrained into the global finance system owned and operated by the same entrenched-money-power that also gains the benefit of the deceit and deliberate mal-education of the masses.

It is only with respect to this uniquely-special-virus called debt-or-loan-interest, that if it grows at an actual rate of 33.3% over 14 days, then the entrenched-money-power that feeds upon it, and otherwise measures financial performance by the basis-point or 1/100th of 1%, will tell you with a straight-face that it is only 435% per annum, even though they are in the business of knowing that it is 180,754%.

The CBC example serves also to expose the psychiatric phenomenon that underlies the nominal method, and which should be readily apparent even to those who otherwise have trouble with the math.

The nominal method is founded upon three clinically-insane propositions:

- The borrower in a loan transaction does not need to know the interest rate defined by the transaction.

- The borrower in a loan transaction does need to know something that is not the interest rate defined by the transaction.

- The borrower in a loan transaction needs to believe that the thing that is not the interest rate is the interest rate.

Substituting the details from the CBC article ($300 for $400, due in 14 days):

- The borrower in a loan transaction does not need to know the interest rate defined by the transaction.

The borrower in a loan transaction ($300 for $400, due in 14 days) does not need to know that the interest rate defined by the transaction is 180,754% per annum.

The CBC article accordingly makes no mention of it.

- The borrower in a loan transaction does need to know something that is not the interest rate defined by the transaction.

The borrower in a loan transaction ($300 for $400, due in 14 days) does need to know something (a nominal rate of 870% per annum) that is not the interest rate defined by the transaction.

The (full) CBC article directly implies that the nominal rate is 870% per annum, but then takes the position that because half the $100 difference is then labelled a loan fee, the interest rate is only 435% per annum. And that requiring half the interest to be paid in advance causes the rate to decline! It’s completely insane. In substance the article implies that the borrower needs to know one of two things – both of which are nominal, and neither of which is the interest rate.

- The borrower in a loan transaction needs to believe that the thing that is not the interest rate is the interest rate.

The CBC article directly provides that the “effective annual interest rate” is 435% per annum, while attributing it to the Financial Consumer Protection Agency of Canada.

So we see also that the Financial Consumer Protection Agency has now also entirely dropped or abandoned the nominal-rate pretence and is now also directly lying by claiming that 435% (and / or 870%) is the “effective [real] annual interest rate”.

But we also see clearly the larger insanity of a system that does not just recognise the three clinically-insane postulates / propositions, but actively acts upon them virtually always and everywhere.

Regardless, after the CBC had directly featured and understated the real interest rate by a factor of 400-times on its national and international website, no one seems to have complained or even mentioned the fact of it.

At this point it should also be noted that none of the financial institutions use the nominal method for internal purposes, nor could they even if they wanted to (except through some form of conversion to the (real) interest rate).

In practice, the sole real purpose of the nominal method is to understate the interest rate to the borrower, and the greater the real rate, the exponentially-greater the relative understatement.

Assume for example, and to make it easy, that you are a micro-lender who has invested $36,500 into 365 different $100 loan contracts. In each case the interest charge is determined in the amount of $1 per day, for each day in the term, and each of the 365 contracts has a different term of from 1 to 365 days.

And so, for example:

The interest rate defined under the first contract with an interest charge of $1 payable after one day is 3,678% per annum.

The interest rate defined under the tenth contract with an interest charge of $10 payable after ten days is 3,142% per annum.

The interest rate defined under the 100th contract with an interest charge of $100 payable after one-hundred days is 1,155% per annum.

The interest rate defined under the 200th contract with an interest charge of $200 payable after 200 days is 643% per annum

The interest rate defined under the 300th contract with an interest charge of $300 payable after 300 days is 380% per annum.

And the interest rate defined under the last contract with an interest charge of $365 payable after 365 days is 365% per annum.

Each of the 365 contracts defines a different rate of interest, and which ranges between 365% per annum and 3,678% per annum.

Yet in all 365 cases the nominal interest rate remains 365% per annum. Why is that?

Because there are 365 days in a year, and that is all that the nominal rate allows you to determine.

And if the interest rate can range between 365% and 3,678% per annum, while the nominal interest rate remains unchanged at 365% per annum, then how can the nominal interest rate be an interest rate at all?

It can’t and it isn’t. It never has been, and it never will be. Technically the nominal rate is a non-exclusive logarithmic derivative “of” the interest rate, and not the interest rate, per se.

For those whose right-brains are more dominant than their left-brains, the nominal method is a purported measuring device for the time-value of money, used almost exclusively for periods of less than a year, that is based on the presumption that money has no incremental time-value for any period less than a year.

Whether expressed mathematically or in words, it is equally and clinically-insane, and the reason regardless why the nominal creditors cannot use it internally, but only use it to misrepresent the rate of interest to the nominal borrower.

Even at the barest technical level, and ignoring all of the criminal law offences, the nominal method is unfit for purpose.

I have not been keeping track of the grand-totals for a few years, but according to the 2016 report from the Financial Health Network in the U.S.:

“This year [2016], we report that financially underserved consumers [mostly the working-poor] in the U.S. spent approximately $173 billion [$173,000,000,000] in fees and interest during 2016 to borrow, spend, save, and plan across 29 financial products in this diverse and continually growing marketplace.”

So in most simple terms, a very disproportionately-large number of the working poor in the U.S. are being systematically looted of at least tens of billions of dollars annually at average interest rates of about 30,000% per annum.

A very disproportionate number of these people are Black, but they are not being looted and exploited because they are Black. They are being looted and exploited because they are poor. The same goes for the disproportionate number of working-poor who are Hispanic. And an ever-growing number and proportion of White people are being systematically looted as they too are just as systemically pushed into the ranks of the working-poor.

If we had real truth-in-advertising there would be signs everywhere that say:

Access to short-term working-capital:

Wealthy Asians: 3% per annum.

Wealthy Blacks: 3% per annum.

Wealthy Hispanics: 3% per annum.

Wealthy Whites: 3% per annum.

Poor Asians: 30,000% per annum.

Poor Blacks: 30,000% per annum.

Poor Hispanics: 30,000% per annum.

Poor Whites: 30,000% per annum.

The real trick being pulled is getting us all to believe that it has much to do with race at all. Actually the real trick is getting us all to not think about it at all.

And the unstated real justification of the entrenched-money-power doing the looting is: But if we told the truth there would be massive social unrest, and so we are really doing everyone here a favour by telling them that the rate of interest is 100-times lower than it really is.

If the reader is confused or not quite grasping what is going on – just think Madoff Investments.

You may recall that Mr. Madoff ran one of America’s premier Wall Street investment companies for 25 years as a naked-Ponzi / pyramid scheme that collapsed with the late 2008 financial panic.